Author: Fernando Lopez

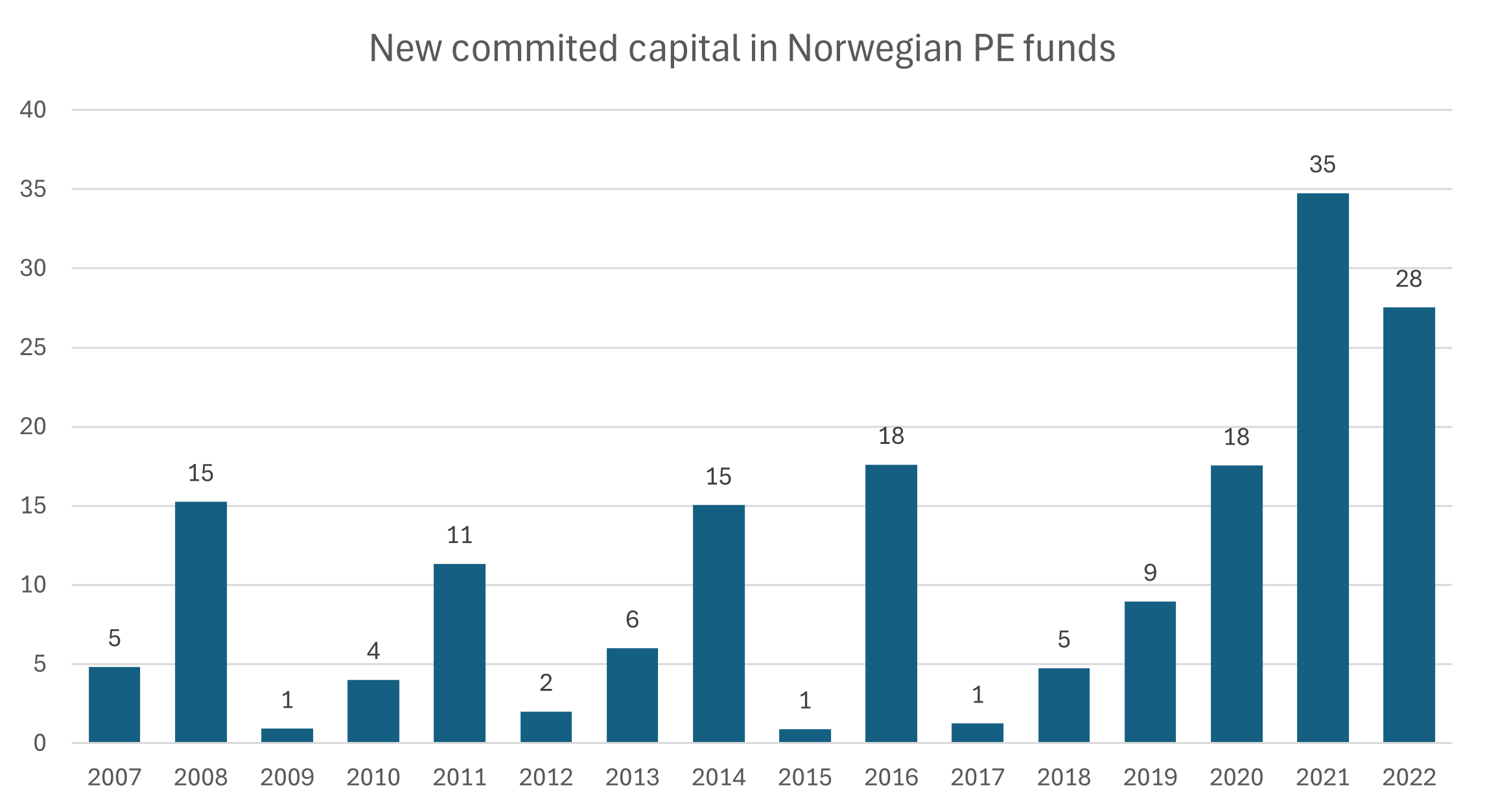

This paper investigates how Private Equity (PE) and Venture Capital (VC) funds operate in practice, guiding readers through both one of the most fascinating and one of the most devastating periods in Norwegian history. It aims to explain the evolution of the PE and VC environments over time. In 2022, the Norwegian PE industry raised 28 billion NOK and invested 19 billion NOK.

This paper is based on research by Menon Economics and Norges Bank, as well as conversations with Private Equity (PE) and Venture Capital (VC) veterans including Tore Rynning-Nielsen, co-founder of Herkules Capital; Gunnar Rydning, co-founder of Verdane (alongside Birger Nergaard); Gisle Østereng, Head of Investments at Startuplab Ventures; and Jan Terje Aasgaard, Head of Private Equity at DNB.

None of what is written is intended to reflect a specific person’s opinion; rather, it is a mix of various discussions and perspectives, supplemented by data from Menon Economics and Norges Bank.

Source: Menon Economics

Assessing PE and VC Funds

Private Equity and Venture Capital are forms of alternative investments, each with its own characteristics and management approaches. These investments are relatively stable with an investment horizon of 5 to 10 years, though this can vary significantly. The funds are organized by Private Equity firms, known as General Partners (GPs), and investors, known as Limited Partners (LPs). Committed capital is used to finance the operations related to fund management and remains locked in by the GPs during the fund’s life. GPs earn money through management fees and performance fees. Specifically, most of the committed capital for PE and VC comes from Pension Funds, High Net-Worth Individuals, Sovereign Wealth Fund and Fund of Funds like Argentum and Cubera.

PE firms usually consist of multiple funds, some targeting specific sectors. For example, Verdane manages several funds such as Capital IV, Capital V, Capital VI, Edda, Edda II, and Idun I, with a specialization in technology. Venture Capital is different in that it finances companies from the ground up, though VC firms also manage multiple funds. In 2024, Startuplab experienced a record deal flow, with 700 startups seeking funding.

Beyond providing passive returns, PE and VC offer additional benefits to investors. Companies invested in by PE funds are as its name suggests private, allowing them to avoid the pressure of constantly reporting quarterly results, unlike public companies that face continuous scrutiny from numerous investors and the media. When assessing a public Private Equity fund like EQT AB, it is evident that most of their income comes from management fees. These fees are intended to cover operational costs and motivate the development of the companies within the fund’s portfolio.

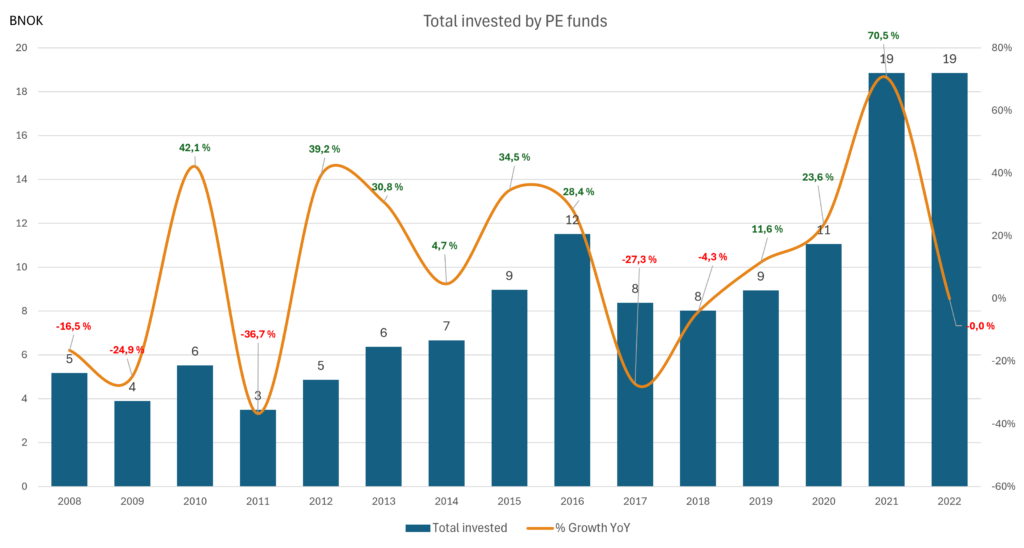

Source: Menon Economics

The Beginnings of PE in Norway

The Norwegian Private Equity (PE) industry emerged from the Venture Capital (VC) industry, which was influenced by the United States. During the 1980s, Harvard, Yale, Stanford, and Princeton led the way in Private Equity investments in the US, breeding a fresh new industry that many aspired to join. As much as 30% of these schools’ total budgets were invested in PE and VC. Gunnar Rydning and Birger Nergaard built Four Seasons Venture from 1986. This period was marked by strong optimism, high investment appetite, numerous startup projects, and high valuations. In fact, the first Norwegian investors in the PE and VC environments were shipping families trying to make a fortune in the US from the early 1980s.

One of the most successful transactions from this era was Gibson Greetings, an American producer of greeting cards. In January 1982, a group of investors acquired the company for $80 million. Of this amount, only $1 million was equity. Sixteen months later, Gibson Greetings went public on the New York Stock Exchange with a valuation of $290 million. After repaying debt, the initial $1 million equity investment exploded to $210 million, representing a return on equity of 20,900%.

The major players in the Norwegian market from the mid 80s included Teknoinvest, Four Seasons Venture, and Origo, with the market capitalization of the Norwegian VC industry amounting to approximately 200 MNOK. Sweden led the way in Venture activity, a trend that continues today. While many industrial corporations now participate in the venture capital industry, it was not a widespread practice at the time. Hydro entered the scene sometime during the 1990s. In Sweden, companies like Saab, Volvo, and Ericsson backed startups and had their own VC departments. The oil industry took a different approach, with Statoil and Equinor serving as technology testers. Unfortunately, Norwegian pension funds were legally prohibited from investing in the industry, a stark contrast to the US where they played a significant role. The first investors in Four Seasons Venture included Fearnleys, ABC Bank and Fred Olsen.

The Grand Norwegian Crash

Overoptimism has never been a good sign, and the Norwegian Venture Capital environment was no exception. The deregulation of capital requirements for banks caused the demand for loans to increase at an unprecedented rate. This period, known in Norwegian as “jappetiden,” saw Young Aspiring Professionals living glamorous lives and asset prices soaring. It lasted from 1984 until 1987.

Gabriel Venture rang the bell at the Oslo Stock Exchange in 1984, backing 15 to 20 startups with a portfolio valued at 140 MNOK. However, just two years later, Gabriel Venture was dissolved. The fact that they were allowed to go public highlights how underdeveloped the Oslo Stock Exchange was at the time.

The real estate market also suffered. Inflation in the country reached 14%, causing prices to skyrocket. People paid 50,000 NOK to skip the line for an apartment in Aker Brygge. Yet, two years later, they were paying to get off the list. Real estate prices dropped by almost 30%, while commercial rents plummeted by 50%.

Jappetiden. Source: NTB SCANPIX (Agnete Brun) / NRK

Have Expected Returns Changed?

During the 80s, Leveraged Buyouts (LBOs) dominated the market. Private Equity (PE) funds could borrow up to 90% of the purchase price while deploying only 10% equity. This low equity injection meant that even modest performance by the private company could translate into highly attractive Internal Rates of Return (IRR). However, times have changed, and so have returns and the structure of LBOs. Today, it is more common to see LBOs with a 50% equity ratio. This ratio can vary depending on the company being acquired, the available assets, and the PE fund’s strategy. As a result, achieving higher gearing is still possible but less common.

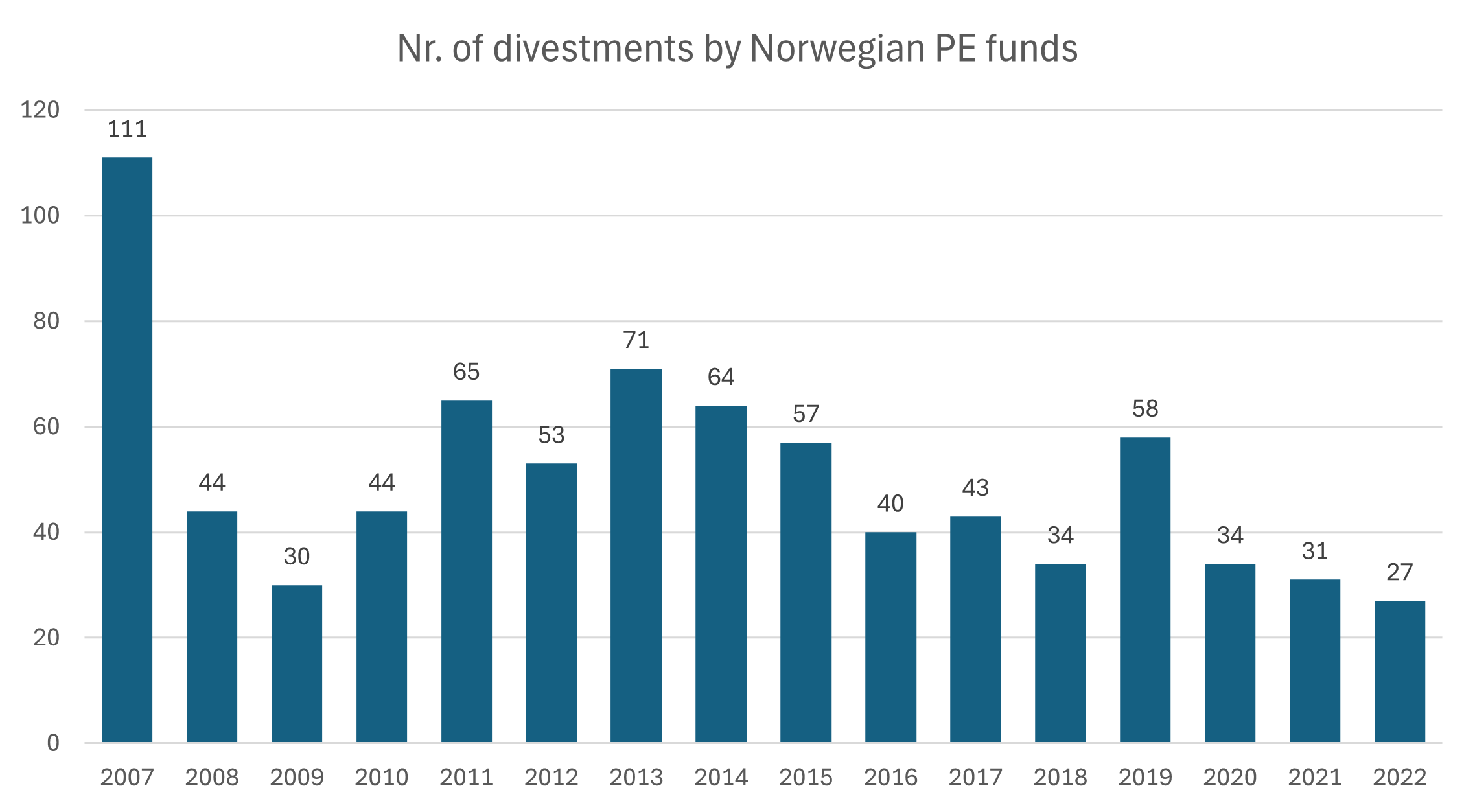

Regarding profitability, the average IRR has decreased from approximately 25% during the 80s and late 90s to 11% from the 2000s, although it still fluctuates. However, the top quartile still continues to deliver IRRs over 20%. Achieving a higher IRR has become more challenging during certain periods due to several factors, one of which is the increased difficulty in executing exits. In fact, the number of exits by Norwegian PE funds has been declining since 2019, reaching an all-time low in 2022.

Source: Menon Economics

Another significant difference between PE and VC now and in the past is the range of industries they invest in. Today, they invest in almost every sector. Take the construction industry, for example. Historically, Private Equity has been reluctant to participate in this sector. However, this has changed in recent years, and investments by PE firms in construction companies are at an all-time high.

Multiple Expansion? Focus on Operational Improvements Instead

Nowadays, many investment funds base their strategies on multiple expansion. This approach involves identifying companies within a specific industry and betting that the industry’s outlook is undervalued. However, this practice is highly speculative, as predicting future multiples is inherently uncertain. In fact, some investors avoid certain funds precisely because they rely on this strategy.

Most agree that the key to investing in a profitable company, aside from having an innovative idea, is effective management. Since the 1980s, operational improvement has become the primary driver of value creation. In contrast, the reliance on leverage and multiple expansion has declined.

Is PE and VC for Retail Investors?

Many PE and VC veterans agree that these types of investments are likely not suitable for retail investors. Firstly, committed capital poses a challenge because withdrawals may occur at inopportune times. In Venture Capital, you typically need around 10 times the invested capital, and companies are highly capital-intensive in their early stages. This means retail investors are likely to be diluted by private placements and new equity issues. In Norway, there are some standout companies like Remarkable and Kahoot. However, returns are likely to be smaller than in other parts of Europe when it comes to VC.

The Future of PE and VC

Consolidation might be on the horizon for the PE industry, resulting in a higher concentration of large Private Equity funds that can deliver IRR in the range of 10-13% . Fewer regional funds will survive, and many may struggle to raise capital again as the cost of maintaining PE funds continues to rise. Previously, it was easier to demonstrate that Private Equity provided superior returns, but now the key lays in enough resources and knowledge about the companies to help them grow and develop. As an investor, it is crucial to be diversified across many funds and industries.

Regarding VC, more stable capital funding from the Norwegian government might be needed to provide stability. Norwegian VC funds that are government-backed experience high volatility in committed capital.

References:

NBIM. (2023). Private Equity. #4. https://www.nbim.no/contentassets/90b5313efab34825a62df9762feb6f29/private-equity.pdf

Menon Economics. (2022). Private Equity funds in Norway. https://nvca.wrep.it/aktivitetsundersokelsen-2022